Before getting started, a quick administrative update to share with the Morrow family — as much fun as I have writing these monthly update letters, unfortunately Time Magazine has yet to extend an offer and until they do, there is a much bigger challenge to tackle. So I’ll be dialing back my aspirational writing career and will write update letters on a quarterly cadence going forward.

Things are starting to pick up a nice pace at Morrow - movement that’s encouraging and exciting. For the first time since starting, balls are rolling with less brute force and, in some cases, on their own. Ironically, many of the more promising, update-worthy developments are still in a infant, pre-announcement stage, so this month’s letter is a cocktail of light updates and heavy enthusiasm.

Jumping right in…

Company updates —

1) Morrow is delivering for early users

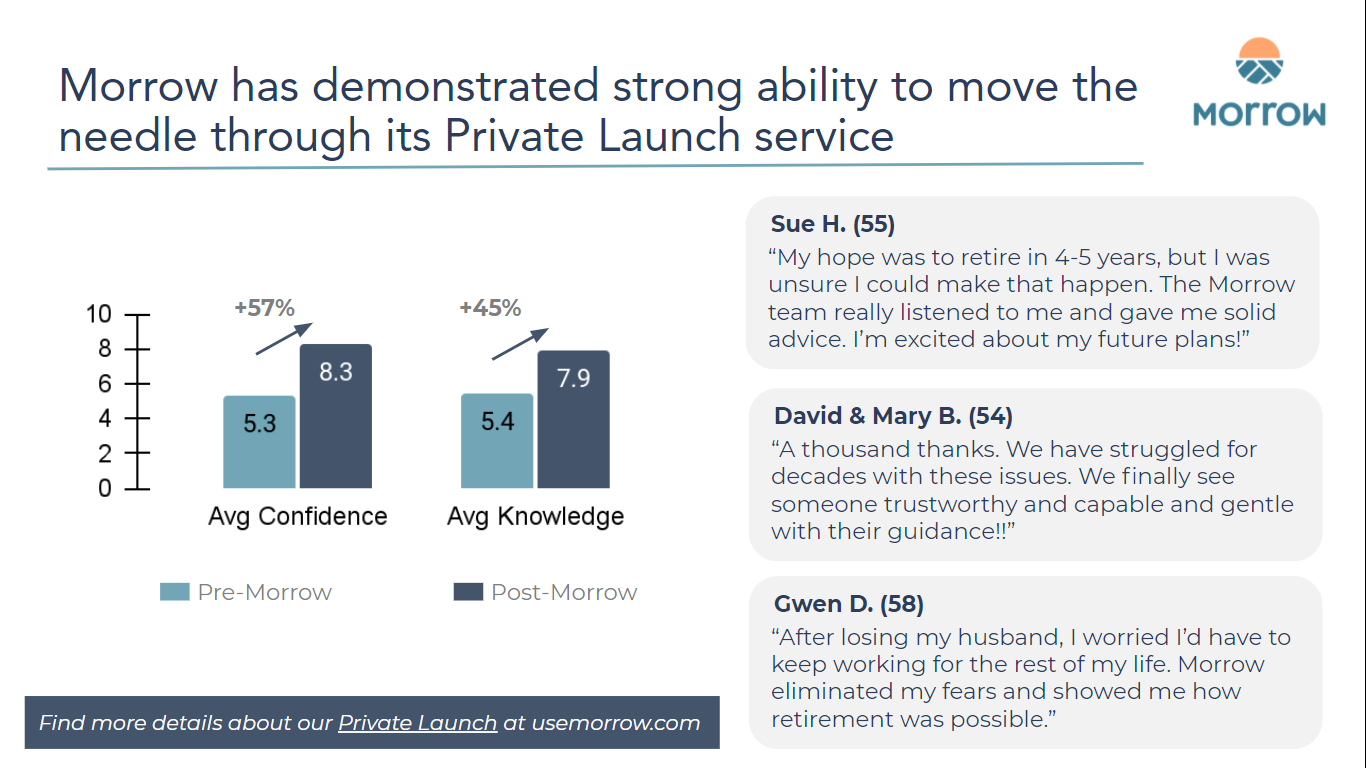

As hoped, our Private Launch program has allowed us to collect quantitative and qualitative feedback that speaks optimistically to the potential impact of Morrow. Early on, strong signals came anecdotally. With the benefit of more time, scale, and user volume, we’ve moved beyond anecdotes and have produced validation on a deeper, more measurable level.

From a product design perspective, we’ve been particularly keen to foster as much intimate target user interaction as our engine for deep learning. Specifically, we have been obsessive over becoming experts on the following questions:

What key retirement questions are asked most frequently? (see Image A)

Can Morrow’s product vision satisfy critical retirement issues? How effectively? (see Image B)

How can Morrow best build product/experience to deliver a new market standard for satisfying critical retirement issues?

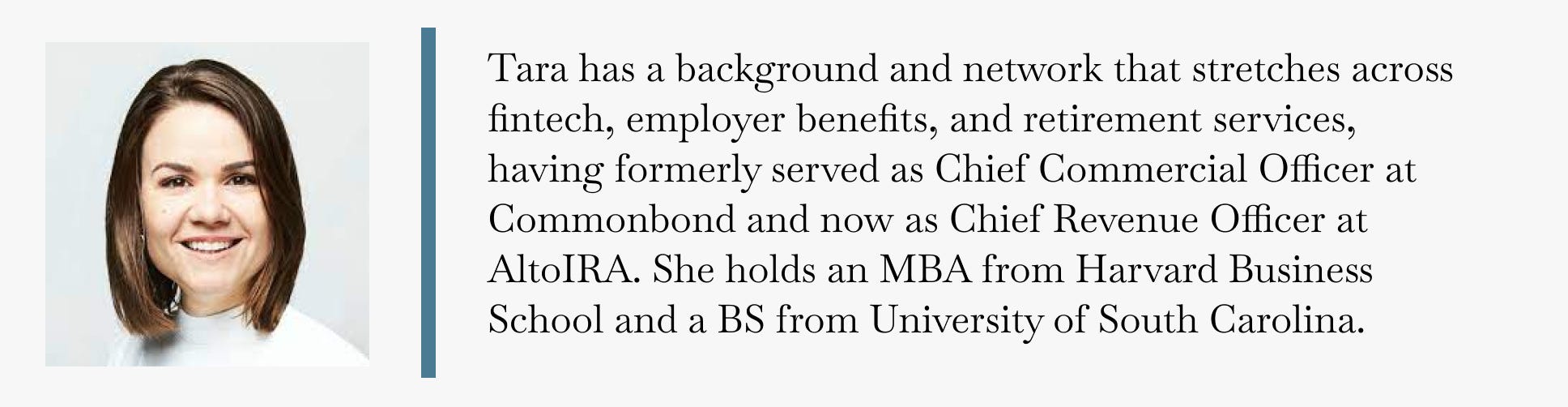

2) Another quality Advisor addition

We’re excited to introduce Tara Fung to our growing team of Advisors. We first met Tara several months back and were struck by her insightfulness facilitated by an extremely rare combo of knowledge and experience base across fintech startups, employer benefit sales channels / contacts, and retirement services. It’s fair to say there aren’t endless people who share that unique cross-section of perspectives. We’re lucky to formally have her aboard!

Tara Fung

Perspectives —

The best summary I’ve read that speaks to our country’s growing retirement crisis is PWC’s Retirement in America: Time to Rethink and Retool. Many of the macro economic beliefs behind Morrow rest on trends outlined in this report. This industry is too consequential at an individual and societal level to fumble along in the dark ages.

Key takeaways:

1) America is wildly unprepared for retirement, a growing and unsettling trend.

“A quarter of US adults have no retirement savings and only 36% feel their retirement planning is on track.”

2) As traditional retirement support systems deteriorate, individual retirement management choices are magnified.

“The US market is more dependent than ever on defined contribution plans (DC). In fact, over 60% of total US retirement assets are now held in such plans, representing a wide scale shift in investment risk from the corporate sector toward employees.”

3) Consumers are calling for more rounded retirement preparation solutions.

“The COVID-19 crisis has highlighted the as-yet-unsatisfied demand among plan participants for a broad suite of financial wellness products that can help them live better lives now as opposed to simple traditional post-retirement planning.

Retirement planning is evolving into an ecosystem of benefits that cross financial planning, health, wellness and financial literacy.”

4) Consumer experience in financial services will dictate market separation.

“As fees fall and margins compress, firms are targeting deals that build scale. Meanwhile, new players — agile, tech-savvy competitors — are beginning to fill in parts of the ecosystem that incumbent retirement firms have neglected. These firms are capturing stickier revenues with a compelling value proposition and a focus on the participant experience.”

“Participants now expect the same always-on technology and highly convenient experiences they find from other industries.”

“The most common factors in selecting a retirement plan provider are strong customer servicing and user-friendly experience — two areas that can be highly differentiated with the right digital approach.”

5) Digital platforms allow an essential mix of scale and engagement. COVID has opened the door to disruption in this respect.

“Digital platforms and mobile apps open additional service channels and allow firms to offer the proper mix of self-service, automated advice and human interaction.”

“Providers might also consider adding new financial wellness modules that extend beyond just education to also include advisor-led or digital advice. Throughout the pandemic, we’ve seen wide adoption of virtual advice models.”

Thanks for tuning in as always :)

— Sammy